FBO accounts sit behind fintech partnerships, embedded finance programs, and corporate treasury use cases. They support clients that need to hold funds on behalf of their customers. Banks that manage them well have a scalable, profitable program banking business. However, banks that manage them on spreadsheets and overnight batch files face a serious operational risk problem. Many may not fully recognize it yet.

At the same time, the compliance burden continues to grow. Regulators are scrutinizing how banks track sub-ledger balances within FBO structures. The 2024 Synapse collapse showed what can happen when that visibility breaks down. Yet many of the systems banks use to manage FBO accounts at scale were never designed for this level of complexity.

In addition, many fintech platforms now pair FBO account structures with B2B virtual cards to control how customer funds are spent and improve transaction-level visibility across payment flows. As embedded finance continues to expand, banks need infrastructure that delivers both operational efficiency and real-time transparency.

Virtual Account Management (VAM) closes that gap. By creating virtual sub-accounts within a single physical FBO account, VAM gives banks real-time visibility, automated reconciliation, and stronger control. It does this without requiring them to replace their core banking system.

The Problem: FBO Accounts and Hidden Complexity

FBO accounts are master accounts that banks hold for program managers, such as fintech companies, to manage funds “for the benefit of” their customers. For example, a digital wallet provider might use a single FBO account at a partner bank to hold the balances of thousands of users. As a result, this structure has become a standard model for fintech partnerships, corporate escrow services, and marketplace payment programs.

While FBO accounts seem straightforward in concept, managing them at scale quickly becomes complex. Every program requires its own ledger to track individual customer balances, transactions, and payment activity. As transaction volumes grow, manually reconciling deposits and withdrawals within a single omnibus account becomes more than a tedious task. It becomes a significant operational risk.

Instead of focusing on higher-value work, operations teams often spend their time reconciling transactions, researching exceptions, and correcting errors. Without real-time visibility, banks cannot accurately determine the balance of each client or program at any given moment. As a result, the risk of commingling funds, misallocating payments, and creating compliance issues increases significantly.

The underlying challenge is simple: most banks lack the infrastructure to segment, monitor, and report on FBO balances at scale. In addition, many institutions struggle to organize transaction data in ways that support automation, reconciliation, and regulatory reporting. As fintech partnerships continue to grow, these operational challenges become increasingly difficult, and expensive, to manage.

The Operational Reality: Why Legacy Systems Fail

Traditional core banking systems were never designed to support modern FBO programs. Although they excel at managing physical accounts, they often struggle to support the thousands of logical sub-ledgers a single FBO account may require. Likewise, they cannot deliver the real-time transaction mapping and granular reporting that banks, fintechs, and regulators increasingly expect.

As a result, banks rely on manual workarounds to bridge the gap. Operations teams maintain spreadsheets as unofficial ledgers, developers build custom middleware to connect disconnected systems, and finance teams reconcile transactions in overnight batches. Consequently, these processes slow operations, increase costs, and create unnecessary risk.

Modern Virtual Account Management (VAM) eliminates these inefficiencies by automating reconciliation and organizing transaction data. It also provides real-time visibility into every virtual sub-account. Instead of waiting until the next business day to understand their cash position, banks and program managers gain immediate insight into balances and transaction activity.

The consequences of relying on legacy infrastructure are clear:

- Increased operational risk: Manual processes and delayed reconciliation introduce a high potential for human error and compliance issues.

- Higher cost to serve: Banks devote more staff and resources to reconciliation, exception handling, and operational support.

- Poor customer experience: Delayed reporting and limited visibility prevent program managers and end users from accessing accurate, real-time account information.

What is Virtual Account Management and How Does it Solve the FBO Problem?

Virtual Account Management (VAM) addresses these challenges by giving banks a modern way to manage complex FBO structures. VAM acts as a logical layer on top of existing physical bank accounts, allowing banks to create and manage thousands of virtual sub-accounts linked to a single FBO account.

Each virtual account functions as a digital sub-ledger connected to the underlying physical account. As a result, banks gain greater cash visibility, automated reconciliation, transaction-level tracking, and flexible account hierarchy management. Instead of relying on manual processes, teams can use real-time data to monitor balances, organize funds, and improve operational control.

Think of it this way: a single physical FBO account can become a structured network of virtual accounts. That network can support thousands of transparent, manageable digital ledgers. Each account can represent a specific end user, program, client, or business entity while maintaining a clear connection to the overall account structure.

In addition, this approach streamlines cash flow management and reconciliation across complex organizations. VAM replaces manual spreadsheet processes with an automated framework that improves accuracy, increases transparency, and delivers real-time visibility into every transaction.

How Virtual Accounts Work

One Physical Account, Thousands of Virtual Accounts

Virtual accounts fix what multiple bank accounts break. Banks know this: managing dozens of physical accounts creates operational headaches, inflates costs, and fragments cash visibility. Virtual accounts solve the problem by creating sub-ledger accounts under a single physical bank account. Companies can spin up thousands of virtual accounts within one master account, each with unique identifiers and flexible hierarchies.

The mechanics are straightforward. Banks create virtual accounts for different business lines, entities, programs, or clients while keeping funds within one underlying physical account. Each virtual account acts as a digital ledger that tracks transactions for a specific purpose or customer.

As a result, payments automatically route to the correct ledger, and transaction data updates in real time. Operations teams no longer need to manually reconcile every payment because the system automatically records activity against the appropriate virtual account.

Real-Time Cash Visibility and Liquidity Management

This approach gives banks a level of cash visibility that traditional account structures cannot match. Treasury teams can view balances and transaction activity across every virtual account instantly, eliminating the need to search through multiple banking portals or wait for end-of-day reports.

As a result, liquidity management becomes more precise because treasurers always know where funds sit and how they move. When cash positions remain transparent, organizations can make better decisions about working capital, forecasting, and fund allocation.

Virtual accounts also simplify account structures by eliminating unnecessary complexity. Traditional banking models often require businesses to maintain separate accounts for every entity, program, or purpose. Instead, virtual account structures consolidate these fragmented setups into a single physical account with logical sub-structures. This reduces account maintenance costs, simplifies credit processes, and creates a more efficient way to manage cash flows.

Operational Efficiency Through Automation

Automation transforms how organizations manage daily account operations. Rather than relying on manual reconciliation and exception handling, virtual accounts automatically assign transactions to the correct ledger and maintain accurate records in real time.

As a result, finance teams spend less time investigating reconciliation issues and more time supporting strategic initiatives. In addition, self-service capabilities allow businesses to adjust account structures as their needs evolve, without waiting weeks for new account approvals.

Virtual Account Management represents infrastructure modernization, not disruption. Banks can deliver enterprise-grade FBO management capabilities without replacing their existing core systems. Ultimately, institutions that adopt this approach can compete more effectively for program banking opportunities that traditional infrastructure cannot support.

Key Benefits of VAM for FBO Structures

A VAM solution directly addresses the limitations of legacy systems while helping banks modernize treasury operations. By improving visibility, automation, and control, VAM enables financial institutions to manage complex FBO structures more efficiently and scale program banking operations with confidence.

- Transparency: VAM gives banks real-time visibility into every sub-account balance and transaction. As a result, banks and their clients can make faster, more informed decisions using accurate, up-to-the-minute data.

- Compliance: VAM strengthens regulatory controls by maintaining clear segregation of funds and generating automated audit trails for every transaction. This helps banks meet increasingly rigorous oversight requirements from organizations such as the FDIC, OCC, and CFPB.

- Reconciliation: Instead of relying on manual payment matching, banks can automate reconciliation processes and significantly reduce errors. Consequently, operations teams spend less time resolving exceptions and more time supporting higher-value activities.

- Liquidity Management: With a complete view of funds across virtual accounts, banks can provide advanced liquidity services, including automated sweeping, sub-account interest calculations, and optimized float management across complex account hierarchies. In addition, VAM supports more efficient treasury operations by improving control over cash positions and movement.

- Scalability: Most importantly, VAM allows banks to support growing numbers of fintech and enterprise programs without a proportional increase in staff or operational complexity. Therefore, it provides the infrastructure banks need to expand program banking capabilities while maintaining profitability.

Use Case Examples

VAM is more than a theoretical concept. In practice, banks and businesses use it across a variety of models to improve visibility, control, and operational efficiency.

Fintech Program Enablement: Sponsor banks can use VAM to create segregated virtual accounts for each end user within their fintech programs. As a result, banks can deliver robust Banking-as-a-Service solutions while maintaining stronger compliance controls, accurate fund tracking, and greater operational oversight.

Corporate Escrow and Marketplaces: Companies that hold funds on behalf of buyers, sellers, clients, or contractors can use VAM to separate and manage those balances more effectively. For example, real estate platforms, franchise networks, and online marketplaces can use virtual account structures to improve transparency and simplify reconciliation across multiple parties.

Corporate Treasury Management: Large corporations can leverage FBO and VAM structures to manage cash positions across internal divisions, subsidiaries, and business units. This gives corporate treasurers a centralized, real-time view of liquidity across the organization.

In addition, VAM can integrate with treasury management systems to support broader financial operations. By connecting account structures with real-time payment data, businesses can improve cash flow management, optimize sales transactions, reduce days sales outstanding, and strengthen financial reporting.

The Regulatory Angle

From a regulatory perspective, Virtual Account Management (VAM) is becoming a necessity. Regulators continue to focus on how banks manage risks associated with third-party payment processors, fintech partnerships, and customer funds. As a result, banks must provide greater transparency, accurate reconciliation, and clear documentation of how they track and protect end-user balances.

Lessons from the Synapse Collapse

Recent industry headlines have shown what happens when that visibility breaks down.

When Synapse Financial Technologies collapsed in 2024, the resulting chaos left tens of thousands of fintech end users unable to access funds. Regulators, banks, and fintechs spent months trying to untangle which funds belonged to whom across multiple partner banks and FBO accounts.

The episode exposed a fundamental weakness in today’s ecosystem: many sponsor banks and fintech platforms lack the systems to track real-time sub-ledger balances and ensure those funds are correctly allocated and safeguarded.

Why Regulators Expect Better Visibility

This is the exact gap that VAM is designed to address. By providing real-time account visibility, automated reconciliation, and detailed transaction tracking, VAM helps banks strengthen operational controls while supporting the transparency regulators increasingly expect.

The Qolo Point of View

At Qolo, we believe FBO management isn’t just an accounting challenge, it’s a visibility and control problem. Traditional VAM solutions are a step in the right direction, but they often operate as yet another siloed system that requires batch updates and external reconciliation.

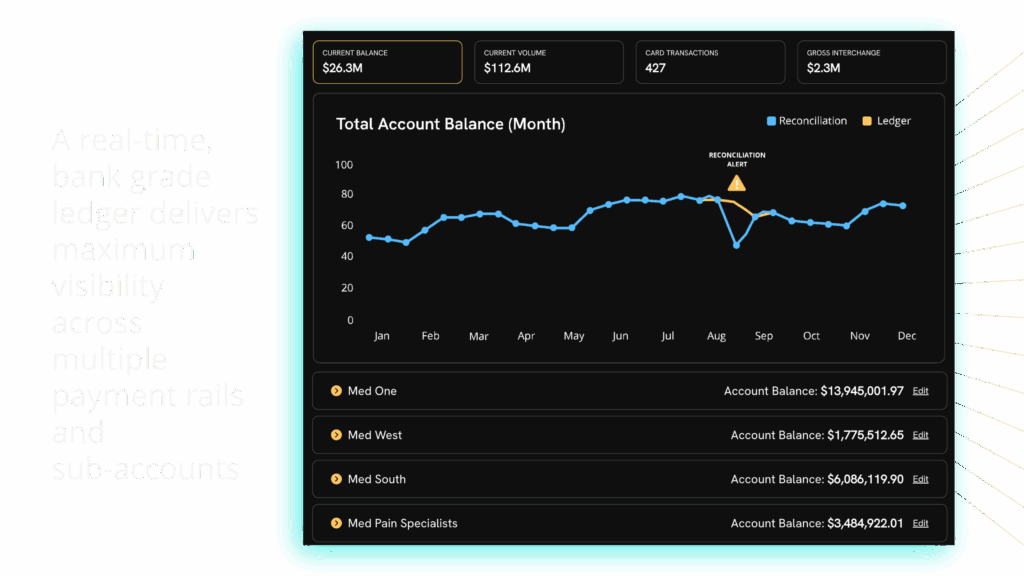

Our Quantum Ledger + Virtual Account Management offers a fundamentally different approach. It is not just an overlay; it is a real-time, bank-grade ledger embedded directly beneath the payments layer. This means that every transaction across multiple payment rails, whether card, ACH, wire or RTP, is instantly reflected in the ledger. There are no batch updates, no data lags and no need for a separate reconciliation process.

In addition, Qolo’s integrated platform combines this powerful ledger with card issuing, processing and money movement capabilities. This provides a single, cohesive infrastructure for managing complex payment flows. For banks, it acts as the real-time, intelligent treasury engine your core system never had. It allows you to compete with agile fintechs and Tier 1 competitors by launching new products and managing money smarter.

Virtual Account Management is no longer optional. It is the infrastructure that enables modern program banking to become more scalable, efficient, and profitable.

Time to Upgrade Your Architecture

If your bank still manages FBO accounts with spreadsheets and overnight batch files, you are carrying unnecessary operational risk and inefficiency. Now is the time to rethink your treasury and sponsor account strategy.

By upgrading your architecture with a modern, embedded ledger solution, your institution can improve visibility, streamline operations, unlock new revenue opportunities, and compete more effectively in the evolving program banking market.

Ready to explore how Qolo’s Virtual Account Management can transform FBO management? Visit our solutions page or contact our team to discuss how real-time ledger infrastructure can support your growth strategy.

Frequently Asked Questions

FBO stands for “For Benefit Of.” An FBO account is a financial account in which funds are held by a bank or financial institution on behalf of one or more underlying customers. While the account may be administered by a fintech, broker, or program manager, the funds are held for the benefit of the end users.

An FBO (For Benefit Of) account allows a fintech, payment platform, or financial institution to hold funds on behalf of its customers in a single account at a bank. While the account is legally owned and administered by the intermediary, the funds belong to the underlying customers. The intermediary maintains detailed records showing how much money belongs to each customer and processes deposits, withdrawals, and transactions accordingly. FBO accounts help fintechs streamline operations, support regulatory compliance, and provide clear ownership tracking without requiring every customer to open a separate bank account.

Both FBO and omnibus accounts can hold funds for multiple customers. However, an FBO account is specifically structured to indicate that funds are being held for the benefit of underlying customers. Depending on how they are implemented, FBO accounts can provide greater transparency into customer ownership and fund segregation than traditional omnibus account structures.

Fintech companies use FBO accounts to simplify customer fund management, reduce operational complexity, support compliance requirements, and enable scalable financial services. FBO structures allow platforms to serve many customers without opening a separate bank account for each user.

The funds in an FBO account belong to the underlying customers, not the fintech or intermediary managing the account. The intermediary administers the account and maintains records of customer ownership, while the funds are held for the benefit of the account holders.

FDIC insurance eligibility depends on the account structure and the financial institution holding the funds. In many cases, funds held in properly structured FBO accounts may qualify for pass-through deposit insurance coverage, provided regulatory and record keeping requirements are met. Customers should review the specific terms of their financial institution or fintech provider.

FBO accounts can improve operational efficiency, simplify customer fund management, support regulatory compliance, and provide clearer ownership tracking. They are commonly used by fintechs, payment companies, and embedded finance providers that need to manage funds on behalf of large numbers of customers.