Financial infrastructure isn’t supposed to be the star of the show. Like good plumbing, when it works, you barely notice it. But when it breaks? Your whole operation floods.

That’s the reality facing banks and fintechs today. Legacy payment systems that once seemed “good enough” are now holding back growth, creating operational headaches, and frustrating customers who expect Amazon-level experiences from their financial services.

Based on insights from Qolo’s Chief Revenue Officer Rouzbeh Rotabi, here’s why enhancing your financial connectivity isn’t just nice to have; it’s business critical.

The “Good Enough” Trap Is Expensive

Many financial institutions think their current payment tools are working fine. But here’s the thing: if you’re constantly hiring engineers, product managers, and consultants just to maintain your existing systems, you’ve hit what Rotabi calls “terminal velocity.”

Ask yourself these questions:

- Are you hiring seven engineers every quarter just to keep the lights on?

- Are you outsourcing more development work each year?

- Is your team spending more time on maintenance than innovation?

If yes, you’re not treading water; you’re sinking slowly. Those aren’t signs of a healthy system. They’re symptoms of infrastructure debt that’s compounding every quarter.

Banks Need More Than Deposits. They Need Deeper Relationships

The banking crisis of 2023 changed everything. Banks aren’t just looking for new customers anymore; they’re fighting to deepen existing relationships and increase commercial deposits. But here’s the catch: you can’t expand your footprint with customers using outdated infrastructure.

Modern commercial clients expect:

- Real-time visibility into their cash flows

- Unified platforms that don’t require juggling multiple vendors

- Seamless integrations with their existing workflows

If you’re asking clients to work around your limitations, they’ll find someone who won’t.

Speed vs. Control: The False Trade-Off

There’s a persistent myth that you have to choose between moving fast and maintaining control over money movement. That’s only true if you’re stuck with fragmented systems.

The reality: You can move quickly when you’re building additive services rather than replacing core infrastructure. Virtual Account Management (VAM), for example, can sit on top of existing banking cores without requiring massive migrations.

The key distinction: Are you creating new capabilities or replacing entrenched systems with daily user experiences? New capabilities can be tested, iterated, and improved quickly. Replacing mission-critical systems requires more careful orchestration.

Infrastructure Debt Compounds Like Financial Debt

Every workaround you build today becomes technical debt tomorrow. Every manual process you maintain becomes a bottleneck as you scale. Every vendor you add creates another potential point of failure.

Modern payment infrastructure should reduce complexity, not add to it. If your current setup requires:

- Multiple APIs for different payment types

- Manual reconciliation processes

- Separate systems for cards, ACH, wires, and real-time payments

You’re not just maintaining the status quo; you’re accumulating infrastructure debt that gets more expensive to fix every quarter.

Your Customers Have Amazon Expectations

Consumer behavior has fundamentally shifted. People carry $1,000 phones that make everything feel instant and effortless. They expect the same from their financial services.

This isn’t about being unreasonable – it’s about competitive reality. If your payment infrastructure can’t deliver smooth, fast experiences, customers will find providers who can. And in B2B markets, those decisions often come with long-term contracts and switching costs that make customer recovery expensive.

The Path Forward: Integration Over Replacement

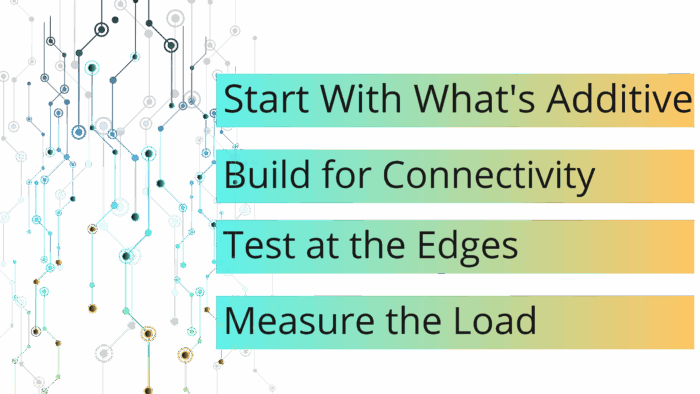

The good news? You don’t have to replace everything at once. The smartest financial institutions are taking an additive approach:

Start with what’s additive: Services like Virtual Account Management can enhance your existing core without disrupting daily operations.

Build for connectivity: Choose infrastructure partners that offer unified APIs for multiple payment types rather than point solutions.

Test at the edges: Launch new services with willing customers who understand they’re getting early access to innovative features.

Measure the load: Track how much operational overhead your current infrastructure creates, then compare that to modern alternatives.

Make Your Infrastructure Decision

If you’re sensing that your platform needs more humans, more vendors, or more workarounds just to maintain current functionality, it’s time to evaluate alternatives. You owe it to your organization to understand what modern infrastructure can deliver.

This isn’t about chasing shiny objects; it’s about building foundations that can support growth rather than limit it. Because in a market where customer expectations keep rising and competition keeps intensifying, “good enough” infrastructure isn’t good enough anymore.

The question isn’t whether you’ll eventually need better financial infrastructure. The question is whether you’ll upgrade proactively or wait until your current systems force the decision for you.

If you’re ready to tackle the challenges of outdated financial infrastructure and unlock new growth opportunities, we’re here to help take the first step toward building a more resilient, innovation-ready future.

To hear Rouzbeh’s full interview on the Finovate Podcast, click here.